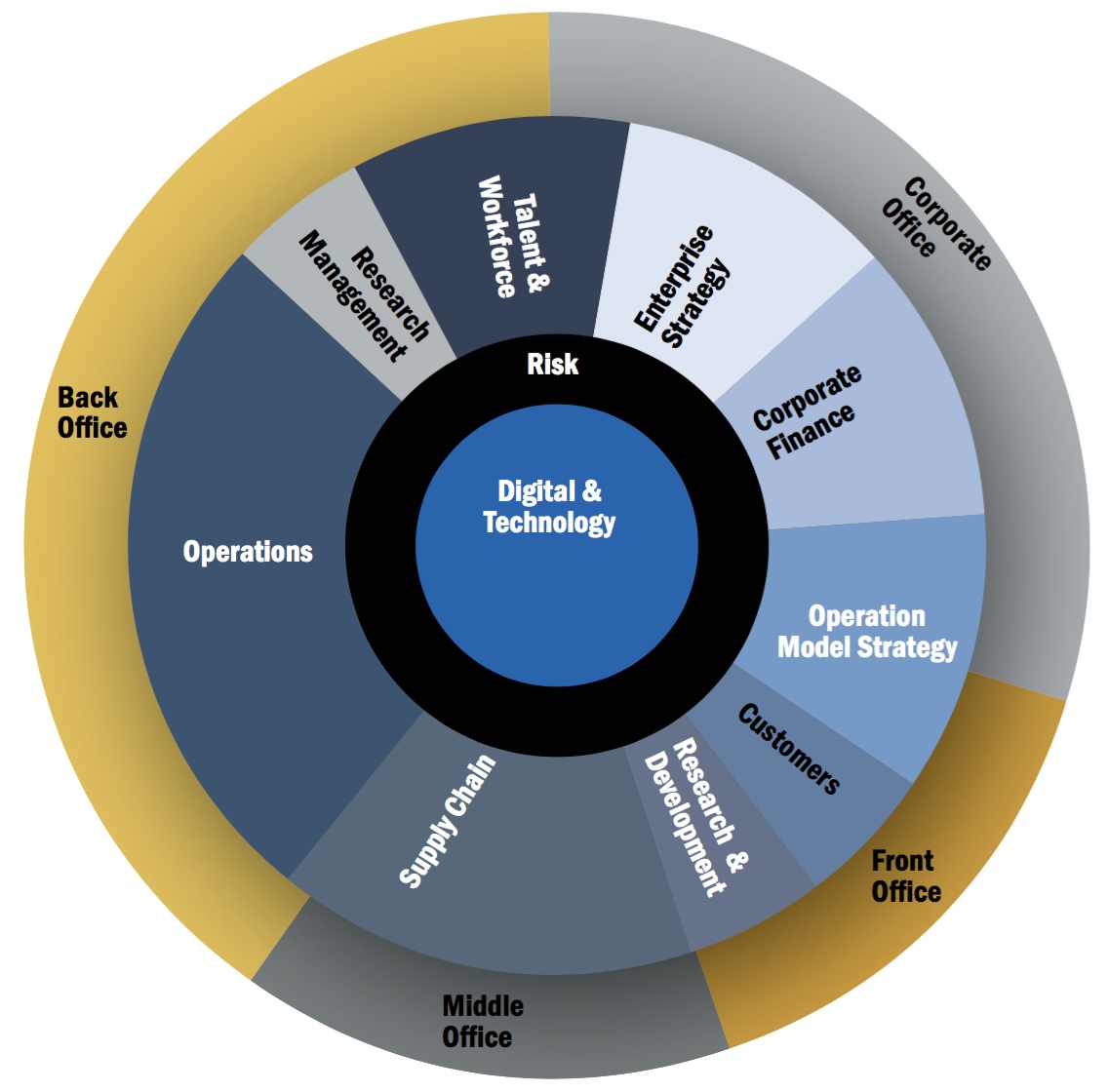

Yearend is opportune for stocktaking. ALM Intelligence introduced in mid-2017 a new taxonomy, which we internally referred to as the "wheel." The conceit was that management consulting was increasingly being delivered as integrated services targeted at cross-functional transformations powered by digitization. The wheel arrayed service spokes against client functions with digital at the hub and risk embedded throughout. This was a departure from ALM's traditional conception of consulting as a loose collection of service pillars that rested on a foundation of industry and geographic practices.

Yearend is opportune for stocktaking. ALM Intelligence introduced in mid-2017 a new taxonomy, which we internally referred to as the "wheel." The conceit was that management consulting was increasingly being delivered as integrated services targeted at cross-functional transformations powered by digitization. The wheel arrayed service spokes against client functions with digital at the hub and risk embedded throughout. This was a departure from ALM's traditional conception of consulting as a loose collection of service pillars that rested on a foundation of industry and geographic practices.

ALM analysts observe much micro-level anecdotal evidence for this integrated service model in their conversations with consultants and clients, but we also assess it at a macro-level through our market sizing and forecasting. Comparing the patterns of growth across the nine services that make up the wheel reveals two distinct periods.

2013-2017: Front to Back Office Transformation

Here are the top and bottom-five of the 36 pair-wise correlations of annual growth rates between 2013 and 2017 for the nine services that make up the wheel. The Top 5 are: R&D-Operations, R&D-Rewards Management; Enterprise Strategy-Corporate Finance, Customer-Rewards Management; and, Customer-Operations. The Bottom 5: Operating Model-Supply Chain; Customer-Supply Chain; Operating Model-Talent; Enterprise Strategy-Supply Chain; and, Supply Chain-Operations. These correlations measure the extent to which the growth patterns of two services tracked closely or not.

The first thing to note is what stayed the same. Among the top-five correlations, the close relationship between Enterprise Strategy and Corporate Finance (M&A) is a longstanding feature of strategy consulting. Turning to the bottom-five, Supply Chain's prominence as an uncorrelated market reflects its legacy as a highly-siloed service targeted at cost performance.

The second notable feature is the rise of the CMO buyer as reflected by four of the top-five growth correlations linking front and back office services. Client companies were squeezed between customer demands for personalization and better experiences, on the one hand, and slowing economic activity, on the other. CMOs moved into the breach by orchestrating integrated, multistep programs designed to free up resources from the back office and reallocate them to the front.

2017-2021: Consolidating the Core

Here are the top- and bottom-five of the 36 pair-wise correlations of annual growth rates between 2017 and 2021. The Top 5: Supply Chain-Talent; Customer-Operations; Supply Chain-Rewards; Rewards-Talent; and, Operations-Talent. The Bottom 5: Corporate Finance-Operating Model; Operating Model-Customer; Operating Model-Operations; Operating Model-Talent; Enterprise Strategy-Operating Model.These reflect one year of actual data together with our forecasts for the next four years. This analysis suggests two ways by which the integrated service model is evolving.

While the linkage between front and back office services continues to be a feature of the market, with Customer and Operations ranking second in terms of the strength of their correlation, the more striking development is the prominence among the top-five correlations of Supply Chain paired with back office services as well as cross-back office combinations. Replacing Supply Chain as the least correlated service is Operating Model (organization design and corporate services consulting).

If ALM's forecasts are correct, one consequence will be a shift of service integration from clients' front office to their middle and back office organizations.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.